Abstract

Rights of first refusals (RFRs) granted to tenants in land privatization auctions enable them to purchase their leased land by accepting the highest bid. RFRs may deter bidders and incentivize non–right holders to adjust their bidding. We conjecture that tenant favoritism with RFRs reduces competition and thus sales prices at the expense of the public sellers. To test the conjectures, we compile a data set of land auctions by two privatization agencies in eastern Germany, one favoring tenants along with an RFR, between 2007 and 2018. Double robust matching results indicate RFR-related reductions in the number of bidders and prices.

- Q15

- D44

1. Introduction

Against the backdrop of soaring prices for farmland, the preemption rights for tenants, neighboring farms, and the state make up the most prominent land market regulation measures, particularly discussed in the European Union (Piet et al. 2012; Swinnen, van Herck, and Vranken 2014; Beaumais, Giannoni, and Tafani 2021; Moog and Bahrs 2021; Vranken et al. 2021) but also in Canada (Lawley 2018) and the United States (Bigelow, Borchers, and Hubbs 2016). In thinly traded land markets, tendering procedures and auctions adopted by both professional and state sellers function as cost-effective mechanisms to find buyers with the highest willingness to pay (Balmann et al. 2021; Seifert, Kahle, and Hüttel 2021). For instance, in line with EU regulation 1997/C209/05, first-price sealed-bid auctions with public tenders have become the predominant mechanism for privatizing farmland. Bidders in these auctions submit sealed bids simultaneously, and the highest bid wins. However, the auction mechanism can result in higher prices compared with search market results (Chow, Hafalir, and Yavas 2015; Sogn-Grundvåg and Zhang 2021). To mitigate the perceived disadvantages of higher prices for local farmers in privatization auctions, various forms of favoritism have been developed, such as restricted auctions (Athey, Coey, and Levin 2013), in which land is reserved for specific bidder groups like organic and young farmers (von Hobe and Musshoff 2021).

In this article, we investigate tenant favoritism in privatization auctions with preemptions rights in the form of a right of first refusal (RFR). This granted right enables tenants to purchase the land they leased at the highest bid. While granting RFRs to tenants may appear to favor right holders (i.e., local farmers), the right holder does no longer have an incentive to submit a competitive bid (e.g., Burguet and Perry 2009). Therefore, all non–right holders have to bid against the anticipated valuation of the right holder instead of the anticipated shaded bid in non–RFR auctions (Choi 2009; Brisset, Cochard, and Maréchal 2020), and the presence of the RFR may reduce their chances of winning. Evaluated against their cost of participating in an RFR auction, a potential non–right holding bidder may decide not to bid (Walker 1999). This limits other farmers’ possibilities for expansion and additional collateral, which is especially disadvantageous for young and start-up farmers (Katchova and Ahearn 2016). Likewise, nonfarmer buyers, such as investors wanting to hedge against inflation and store wealth, may not participate. Because the absence of competitive bids from the right holder and other potentially deterred bidders in the price discovery process may imply less competition, public sellers may suffer from lower prices and losses compared with non–RFR auctions (see Krishna 2009).

Other price effects related to tenant favoritism with RFRs may result from the adapted bidding behavior of non–right holders. Under asymmetric bidder structures and risk neutrality, or different degrees of risk aversion, the right holder as the weaker bidder appears favored by the RFR. Both theory (Lee 2008; Brisset, Cochard, and Maréchal 2020) and experimental evidence (Brisset, Cochard, and Maréchal 2015) show that non–right holders may bid more aggressively. Although the consequence of reduced competition suggests lower prices in RFR auctions, it is possible that more aggressive bidding may lead to higher prices.

To our knowledge, there is some anecdotal evidence of the effect of RFRs on the outcome of single auctions (e.g., Lee 2008). For the land market, a comparison by Hüttel, Wildermann, and Croonenbroeck (2016) of the search market with auction results in the same region we use does not causally associate the price differentials between the search market and auctions to tenant favoritism. We undertake a quantitative causal investigation of the effects of tenant favoritism with RFRs on competition and auction results. Based on our review of the auction literature, we hypothesize that tenant favoritism with RFRs reduces overall auction competition and the resulting sales prices at considerable cost to the public.

We compile an extensive data set of farmland privatization auctions held by two agencies in the federal state of Saxony-Anhalt in eastern Germany in 2007–2018. One acts as the rural settlement agency and privatizes the land of former states on behalf of the federal state, where the other acts as state privatization agency across all eastern Germany regions and privatizes the land collectivized and expropriated on behalf of the federal ministry of finance. The rural settlement agency favors tenants by granting RFRs and timely exclusive information about upcoming tenders, and the state privatization agency does not. Other differences between agencies include their tender strategies, where the “counterfactual agency” (without tenant favoritism) publicizes tenders widely, whereas the rural settlement agency (with tenant favoritism) acts locally. Comparing the two agencies’ auction results under the same regulatory framework of farmland markets and the implementation of the EU Common Agricultural Policy, both organized at the federal state level in Germany, should elicit the effects of tenant favoritism with RFRs on competition and sales prices.

Adopting a double robust matching approach with matching as the preprocessing step (Ho et al. 2007), we use the privatization agency’s auction results (without tenant favoritism) to estimate the counterfactual auction results of the rural settlement agency supporting their tenants. Using postmatching regressions as the second step, we quantify the effects attributable to the RFR on competition measures and sales prices. Finding on average reduced competition as indicated by fewer numbers of bids and fewer non–right holding bidders supports our conjecture that the RFR has a deterring effect. We also find lower prices in RFR auctions compared with non–RFR auctions.

To our knowledge, we provide the first empirical evidence of tenant favoritism (granting RFRs) on the outcome of farmland auctions. Since there are only a few empirical evaluations of the farmland policy measures designed to protect local farmers,1 our findings may help develop ways of supporting tenants concerned about being priced out of the market, nonsustainable management practices, and other perceived issues related to nonagricultural investors’ activities in farmland markets (Kay, Peuch, and Franco 2015; Desmarais et al. 2017; Brady et al. 2017), and potentially assist policy makers in improving farm security policies throughout the European Union and elsewhere.

2. RFR Effects in Land Auctions: Auction Theory and Conjectures

Bidder Behavior in First-Price Sealed-Bid Auctions without RFR

Both agencies privatize former state-owned land by using first-price sealed-bid auctions with public tenders without binding and reported reservation prices. We follow Perrigne and Vuong (1999) and the land auction-specific considerations in Croonenbroeck, Odening, and Hüttel (2020). We base our theoretical considerations on the independent private value (IPV) paradigm under symmetry and risk-neutral bidders.2 We also consider potentially affiliated values and asymmetries between bidders when discussing the RFR’s effects using the IPV results as a benchmark.

The optimal bidding strategies in first-price auctions derive from a utility maximization problem, where utility U = U(ν) is a function of the bidder’s private information on the valuation of the land, ν. We model the valuations as random variables with realizations ν. We assume that bidders have symmetric information and other bidders’ private information are uninformative for the bidder such that U(v) = ν. We also assume that all bidders assess the relationship between their bid and the probability of winning, and engage in incentive-compatible behavior (bidder rationality). Each bidder relies on strategy σ(·) that maps a private value to the bid b. For auctions with at least two bidders, at the Bayesian Nash equilibrium, each bidder chooses the bid that maximizes their expected profits subject to the boundary condition  , where

, where  denotes the lower bound of the value distribution. The solution is given by a first-order differential equation describing the bidding strategy as a function of the valuation, its distribution, and the number of bidders (see Perrigne and Vuong 1999 for details).

denotes the lower bound of the value distribution. The solution is given by a first-order differential equation describing the bidding strategy as a function of the valuation, its distribution, and the number of bidders (see Perrigne and Vuong 1999 for details).

Bidders aim to outbid their competitors with the lowest bid possible to maximize their expected payoff (e.g., Krishna 2009). Starting from a maximum willingness to pay equal to the bidder’s valuation for the land, we assume that bidders place a bid below their valuation (otherwise known as bid shading) to ensure positive profits, and no bidders place a bid above their valuation because then the resulting profit would always be negative. To choose the payoff-maximizing bid, bidders form expectations about their competitors’ bids. We formulate a bidder’s expected profit in first-price auctions as:

1

1

where p(b) denotes the probability of winning with bid b. By estimating their competitors’ bids, each bidder faces a trade-off between the probability of being the highest bidder and the possible payoff. Making higher bids increases the probability of winning and reduces the possible payoff simultaneously.

Effects of the RFR in First-Price Auctions

By granting the RFR to one bidder, the right holder can buy the land by paying the highest price the seller is able to get from the other bidders. To account for the effects attributed to favoring one bidder by the RFR in the participation and bidding strategy, we follow Arozamena and Weinschelbaum (2009) for independent private values, Choi (2009) for affiliated private values, and Burguet and Perry (2009) generalizing the results of Choi for multiple buyers. Because of the RFR, the right holder does not need to participate in the price discovery process; thus, bidders no longer determine their bidding strategies simultaneously. After non–right holders submit bids, the right holder evaluates the highest bid and decides whether to exercise the RFR. We formulate the buy-refuse decision as:

2

2

where bRH denotes the right holder’s bid, vRH denotes the valuation of the right holder, and  denotes the highest bid of any other bidder. The right is exercised if the right holder’s valuation vRH exceeds

denotes the highest bid of any other bidder. The right is exercised if the right holder’s valuation vRH exceeds  and the right holder pays

and the right holder pays  ; otherwise, the bidder submitting

; otherwise, the bidder submitting  wins. The right holder’s optimal strategy depends on the other party’s bid, where closed-form solutions for this bid remain difficult to obtain (Arozamena and Weinschelbaum 2009; Choi 2009; Brisset, Cochard, and Maréchal 2020).3

wins. The right holder’s optimal strategy depends on the other party’s bid, where closed-form solutions for this bid remain difficult to obtain (Arozamena and Weinschelbaum 2009; Choi 2009; Brisset, Cochard, and Maréchal 2020).3

Granting an RFR implies that non–right holders can only acquire the land if their bids exceed the valuation of the right holder, unlike standard first-price auctions (our counterfactual), in which competitors compete against the shaded bid and not against the right holder’s valuation (Burguet and Perry 2009). Thus, the RFR makes non–right holders worse off because the right reduces their expected profits and generates a negative externality.

Because of the negative externality, the RFR may deter non–right holding bidders and thus constitute a barrier to entry. Also, the non–right holders’ potential costs of bid preparation and information gathering may outweigh their already reduced expected profits of the non–right holding bidders (Walker 1999; Bikhchandani, Lippman, and Ryan 2005; Brisset, Cochard, and Maréchal 2020). Walker (1999) argues that potential bidders may decline to bid against an insider holding an RFR for two reasons. First, because for almost all cases in which the right is applied, the right holder is in a special relationship to the offered object and may have idiosyncratic values that increase the willingness to pay. Second, as an insider, the right holder may have informational advantages about the valuation of the offered object. The right holder exercises the right up to the believed true value of the object; otherwise, the right holder refrains and the non–right holder wins. Under these circumstances, for a non–right holder winning against a better-informed insider may be “bad news” and can result in the winner’s curse. We note that the RFR can mitigate the winner’s curse for the right holder but make it worse for non–right holders (Choi 2009).

If non–right holders are not deterred by the RFR and other forms of favoritism, in single-object auctions with risk-neutral bidders and symmetric valuations, they have no incentives to bid more aggressively in first-price sealed-bid auctions with RFRs (Arozamena and Weinschelbaum 2009). Assuming that an RFR does not affect the non–right holders’ bidding strategies, granting an RFR for free cannot benefit a seller in terms of sales price due to less competition: the seller suffers from a competition effect because of the absence of the right holder’s bid (Brisset, Cochard, and Maréchal 2020) that can be aggravated by deterred bidders and negatively affects prices (Brannman, Klein, and Weiss 1987; Bulow and Klemperer 1996; Krishna 2009).

Departing from the assumption of risk-neutral bidders, Brisset, Cochard, and Maréchal (2020) show that a risk-averse bidder facing an RFR may bid more aggressively compared to first-price auctions without the RFR. Furthermore, potential asymmetric bidder structures regarding their valuations, such as the different financial constraints we expect in our setting, may alter bidding behavior in first-price auctions even without the RFR. Facing a strong bidder may serve as an incentive for a weaker bidder to place a bid closer to its own valuation, whereas stronger bidders may bid less aggressively (Campo et al. 2011). Granting RFRs to the weaker but favored bidder group may level the playing field between the weaker and stronger bidders and incentivize the stronger bidder to bid more aggressively (Lee 2008). In this case, the non–right holders may bid aggressively to compensate for the (perceived) disadvantage by the RFR (Lee 2008; Arozamena and Weinschelbaum 2009; Burguet and Perry 2009; Brisset, Cochard, and Maréchal 2020).

Taken together, the reduced competition by the RFR may reduce prices but more aggressive bidding behavior by non–right holders may counteract. The effects appear simultaneously, where disentangling competition and both types of price effects empirically require detailed information and a structural estimation of auction data. Because our data set does not offer sufficient detail, we focus on the net effects on competition and prices.

Overall, for the right holder and the seller, the RFR increases ex ante their joint profit by transferring potential rent from an unfavored third party (parties) (Arozamena and Weinschelbaum 2009; Burguet and Perry 2009; Choi 2009). Whereas first-price auctions are efficient regarding the allocation (Krishna 2009), the right allows inefficiency through rent extraction. That is, the right holder can win despite not having the highest valuation among bidders. Thus, without any countervailing welfare enhancements, granting the RFR may result in welfare losses for society.

Conjectured Competition and Price Effects of Tenant Favoritism with RFR in Land Auctions

Based on our review of the existing theoretical models, we expect two effects related to competition and two related to prices. First, when the right holder has no incentive to submit a competitive bid, we call this first effect the pure competition effect (Brisset, Cochard, and Maréchal 2020). Our first competition conjecture is C1a: land auctions, in which the seller grants an RFR to the tenant, differ by at least one competitive bid from land auctions in which the seller does not grant an RFR (competition effect).

Second, since an agency’s grant of an RFR to a tenant is common information, potential bidders may decline to bid against the right holder’s valuation (Walker 1999). Moreover, a tenant may place a higher value on the leased land because, for instance, losing the land may induce reallocation costs or changes in borrowing constraints because of the losses in collateral with potentially increasing capital costs (Weber and Key 2015). As noted, forming a bid is costly: besides information gathering, financing approval must be submitted to both agencies (Hüttel, Wildermann, and Croonenbroeck 2016). For the same cost and benefits, however, the lower chance of winning in an auction with an RFR may deter potential bidders. When an RFR becomes a barrier to entry for non–right holders, we call this second effect the deterrence effect of the RFR. Our second competition conjecture is C1b: fewer non–right holders bid in land auctions granting an RFR to tenants compared with auctions without an RFR (deterrence effect).

Due to the missing incentive for the right holder to submit a competitive bid (competition effect) and the expected deterrence effect, less competition in the price discovery process may lead to lower winning bids (prices). We call this an indirect price effect of reduced competition (Figure 1).

Effects Attributable to Tenant Favoritism Based on Auction-Theoretical Considerations and Conjectures to Be Investigated Empirically

Because of potential asymmetries and potentially affiliated valuations in our study’s farmland market, tenants may appear as the weaker bidder group, and favoritism signals the protection for this group. In this case, non–right holders may need to readjust their bidding strategies and bid closer to their valuations. For instance, investors having fewer financial constraints that potentially outweigh the informational disadvantages about local farmland market conditions, may constitute a group of stronger bidders (Clapp and Isakson 2018; Seifert, Kahle, and Hüttel 2021). While the asymmetries between bidders’ different legal forms and between former tenants and other bidders do not appear to influence winning bids systematically in our counterfactual auctions (Croonenbroeck, Odening, and Hüttel 2020), nontenant farmer (investors) bidders as non–right holders may compensate for tenant favoritism with the RFR by bidding more aggressively, particularly for lots offering higher future returns. Ceteris paribus (i.e., without the competition effect), in these first-price auctions, higher prices may result.

Both competition-related effects lead to lower prices, whereas the adjusted bidding strategies in the case of asymmetries may result in higher prices (Figure 1). As noted, because the effects appear simultaneously, we can only observe the results of both. Effects equal in size would appear a zero-price effect. In auctions with fewer bidders, as in our setting, we expect the competition effect to gain relative importance; for instance, for our counterfactual sample, one less bidder already suggests a reduction of the number of bids by more than 25% on average. Furthermore, if direct price effects attributable to increased bids of non–right holders would exceed the indirect, competition-related price effect attributable to the competition effects, a bidder could then bid over their private valuation, which would be irrational (Crawford and Iriberri 2007). Thus, on average, we expect price markdowns in auctions with tenant favoritism and the RFR; we call this the net price effect. Our first mean price conjecture is C2a: land auctions granting an RFR for tenants receive lower winning bids on average compared with auctions without an RFR (net price effect).

Assuming that a lot characterized by excellent soil quality and so on attracts more bidders aware of these qualities, we expect the deterrence effect to have little influence in RFR auctions. This is because bidders can anticipate the higher competition, and suitable substitutes offered by other sellers may be especially rare ceteris paribus resulting in more aggressive bidding, irrespective of the seller. Also, with potential asymmetric bidder structures and related potentially more aggressive bidding in RFR auctions, we expect even less influence of the deterrence effect and thus a lower price effect in these auctions. Therefore, under more bidders, we expect the price differential to be lower or even absent. We call this fourth effect the asymmetry effect and our second price conjecture is C2b: the difference in winning bids (prices) between auctions attributable to tenant favoritism with an RFR decreases with the respective auction’s number of bidders (i.e., asymmetry of price effects).

3. Empirical Setting and Data

Land Privatization in Saxony-Anhalt

The farming structure and farmland market in Saxony-Anhalt is characterized by the post-communist transition starting with Germany’s reunification in 1990 (see Wolz 2013; Hartvigsen 2014). The rural settlement agency LGSA privatizes the land of former state farms on behalf of the federal state of Saxony-Anhalt, and the federal privatization agency BVVG privatizes the former collectivized and expropriated land on behalf of the German federal ministry of finance. Why a parcel is privatized by LGSA or BVVG mainly relates to previous ownership, location, time, and type of collectivization or expropriation (Wilson and Wilson 2001; Wolz 2013). For instance, LGSA parcels are mainly restituted lands formerly owned by municipalities and state domains that were historically located in the center of the federal state (Löhr 2002; Schmidt 2009; Hüttel et al. 2013; Langenberg and Theuvsen 2016).4 LGSA’s average land market share is about 5%, and BVVG auctions make up about 10% on average between 2007 and 2018 (see Appendix Table A1). However, land markets in Germany and Saxony-Anhalt are thinly traded; the traded volume in 2019 was less than 1% (StaLa 2021).

In line with German privatization principles and EU legislation, BVVG relies on public tenders with a first-price sealed-bid auction mechanism to privatize at market prices (Hüttel et al. 2013). Tenders are published online, and auctions are advertised in farmers’ magazines along with information about the lots. Bidders are invited to submit sealed bids and proof of financing up to a fixed deadline. The highest bidder is awarded the contract for a price equal to the bid. BVVG also publishes the last six months of auction results on its website (BVVG 2020).

BVVG does not communicate reference prices, but it does reserve the right to repeat an auction if the internal reference price is not obtained (Croonenbroeck, Odening, and Hüttel 2020; Seifert and Hüttel 2023). Lot sizes should not exceed 15 ha; prior to 2013, the maximum lot size was about 50 ha. Lots smaller than 10 ha must be auctioned when the lease contract expires. The German federal ministry of agriculture obligates BVVG to conduct restricted tenders for labor-intensive farming systems and organic and young farmers; beginning in 2005, the volume is around 10% of all auctions (von Hobe and Musshoff 2021).

As the rural settlement agency, LGSA acts independently, although the federal state of Saxony-Anhalt is its main shareowner. LGSA’s aim is to strengthen rural areas (Langenberg and Theuvsen 2016; LGSA 2020). It prefers selling to farmers and supports tenants by granting them RFRs designed to support local farmers. When financing a purchase is a barrier to entry, LGSA provides additional qualitative support (e.g., timely announcements so that tenants can prepare to participate, financing sources, and a target lot size of tendered land not exceeding 10 ha to maintain tractability of financing management for farms). Like BVVG, LGSA uses first-price sealed-bid auctions with public tenders and provides detailed information, although it relies on a less strict privatization schedule and even adapts tenders depending on land market situations and tenants’ economic situations. If a tenant shows interest but has temporary liquidity constraints, LGSA may extend the leasing contract and postpone the tender.

Since 2000, LGSA has had a tenant support structure, which is likely to be common information. Non–right-holding potential bidders may view a tender as a signal that a tenant with a high valuation is participating without being a bidder. In this case, the potential bidders may decline to bid against the tenant owning an RFR because the right holder and current user of the land is in a special relationship to the offered land and may have idiosyncratic values that will increase the tenant’s willingness to pay (Walker 1999).

Another qualitative difference between the two agencies concerns the target buyer groups. LGSA’s preference to sell to farmers does not exclude farmer investors. This preference seems rather informal and may not be common knowledge among all potential bidders, particularly in our data set’s early years (after 2007). Although BVVG and LGSA share a pool of potential bidders, LGSA’s preference for farmers may have gradually contributed to the deterrence effect defined in C1b.

It is also possible that bidders may decide to participate in auctions conducted by BVVG, mainly because of the RFR, or because BVVG’s professionalism and experience signal a lower likelihood that the auction will be repeated. Repeating an auction is generally less favorable to potential bidders because they have to resubmit bids, incur transaction costs, and run the risk of higher prices. In this article, we expect that such selection issues will be less relevant, given market thinness, scarcity of land, and missing substitutes.

The group of farmers denotes the largest group of potential bidders in the region. In 2016, nearly 4,440 farms cultivated on average 270 ha (MULE 2019), of which privates farms operated on average 180 ha and accounted for approximately 65% of the farms.

Cooperatives and legal entities operated on average 373 ha and 787 ha, respectively, and cultivated around 70% of the agricultural land in 2016. Characterized by low livestock density (Destatis 2017), Saxony-Anhalt’s agricultural sector has less demand from livestock farms for manure regulation within the nitrate directive compared with western regions in Germany (Breustedt and Habermann 2011).

After the global financial crisis in 2008, agricultural and nonagricultural investor interest in farmland increased in Saxony-Anhalt (e.g., van der Ploeg, Franco, and Borras 2015; Hüttel, Wildermann, and Croonenbroeck 2016). Nonfarmer buyers represent the second-largest buyer group. Investor buyers may purchase land as mid- to long-term investments to hedge against inflation, store wealth, and generate steady income streams by leasing the land and for speculative purposes with capital gains from resale (Magnan and Sunley 2017; Visser 2017). Curtiss et al. (2021) argue for classifying the buyer group as financially strong, and Tietz, Forstner, and Weingarten (2013) note that a considerable group of farmer investors aim to store wealth. The group of nonfarmer buyers may also include farming start-ups and buyers acquiring land for private uses (e.g., horse breeding). For the latter, smaller lots near residential areas are usually of interest (Ritter et al. 2020).

Both farmer and nonfarmer groups may form a group of strong buyers with lower financial constraints. These non–right-holding bidders potentially interested in highly attractive lots may bid more aggressively even knowing about the qualitative support provided to tenants, compared to bidding in auctions without RFR, to compensate for their perceived disadvantage. Their aggressive bidding may contribute to the asymmetry effect defined in C2b.

Data

The initial data sets cover 2007–2018, with 1,009 (1,405) LGSA and 1,940 (10,756) BVVG auctions in Saxony-Anhalt (total). To increase the pool of control observations, we also consider 2,417 BVVG auctions in the neighboring regions of Saxony-Anhalt. To consider only comparable types of auctions, we exclude 485 restricted tenders of the BVVG. We rely on competitive auctions with at least two participants (Croonenbroeck, Odening, and Hüttel 2020). We define a participant as a potential winner in the tendering process (i.e., all of the bidders who have submitted a bid or may purchase land through the RFR). Therefore, for BVVG, we exclude 636 auctions with one bidder. For LGSA, presuming that non–right holders must bid against the right holder’s valuation, we also consider 16 auctions with one bid submitted by a non–right holder; 38 auctions where the tenant as the right holder is the single bidder are excluded.

We exclude 31 LGSA and 3 BVVG observations with missing values in variables describing land or auction characteristics. Using the minimum covariance determinant estimator for outlier detection (Rousseeuw and van Driessen 1999), we exclude 274 auctions (14 LGSA, 260 BVVG). The final data set contains 3,899 observations: 926 by LGSA and 2,973 by BVVG, of which 1,337 are in Saxony-Anhalt.

For an auctioned lot, we use lot size; soil quality measured by the soil quality index;5 share of arable, grassland, and other land and location at the Gemarkung,6 Germany’s smallest administrative unit; bid submission deadline; winning bid; and number of submitted bids. For LGSA auctions, we observe whether the tenant exercises the RFR or wins by its own bid.

As reported in Table 1, lots auctioned by LGSA are on average larger (7.38 vs. 4.92 ha), with higher shares of arable land (87% vs. 69%) and higher soil quality than lots auctioned by BVVG. LGSA’s average soil quality of 67.2 is slightly above Saxony-Anhalt’s average soil quality index of 60, whereas BVVG’s soil quality of 50.2 is below the average, although it ranges from the worst to the best qualities available in Saxony-Anhalt (StaLa 2021).

Descriptive Statistics of LGSA and BVVG Land Auctions, 2007-2018

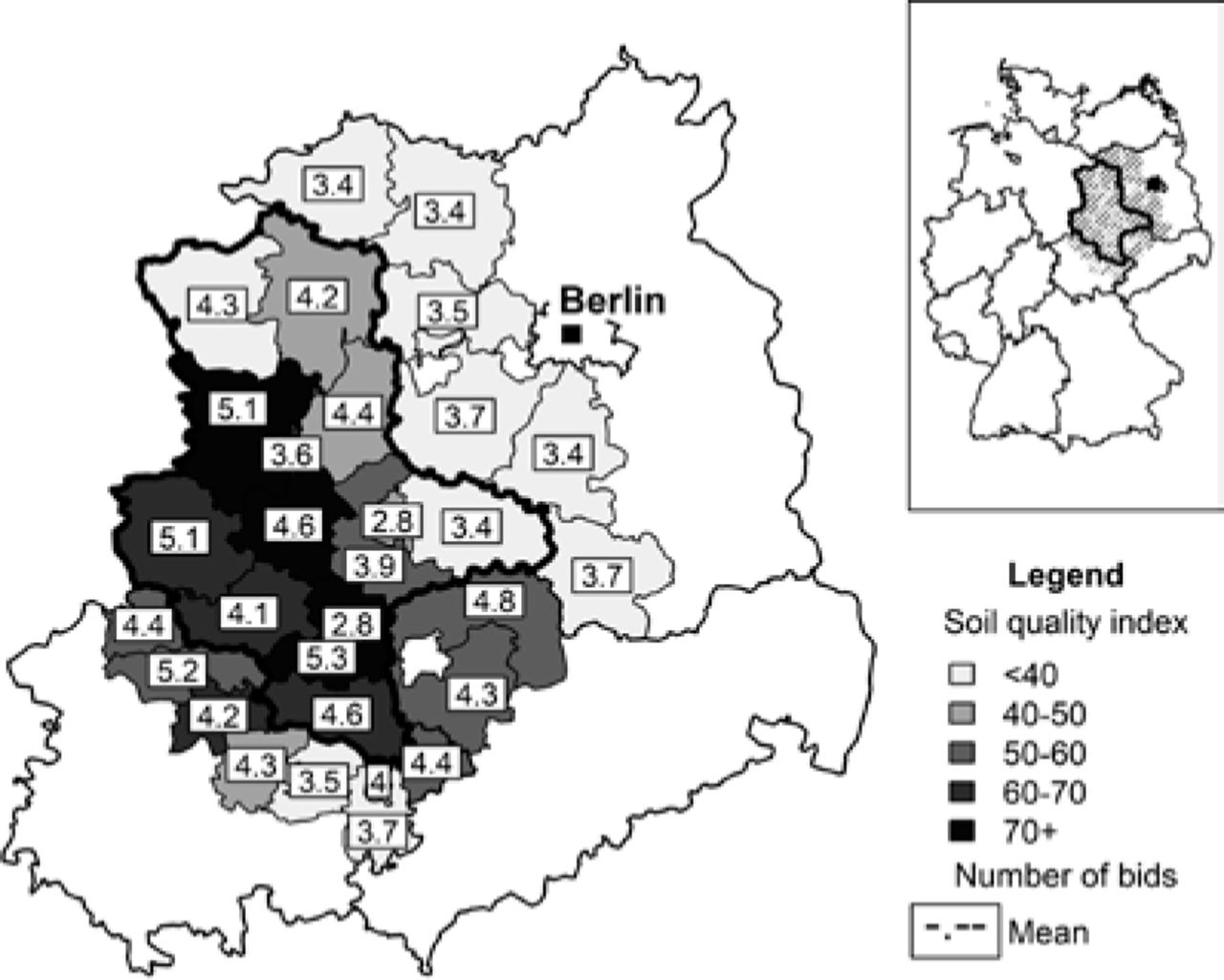

Both LGSA and BVVG receive up to 13 bids in an auction. Both agencies have similar means, with 4.52 bids on average in LGSA auctions and 4.22 in BVVG auctions. As shown in Figure 2, the average number of bids per auction reveals some spatial variation, where data show a higher number of bids for auctions with high soil quality.

Average Soil Quality and Average Number of Bids by County

In about 73% (680) of the LGSA auctions, we observe a bid by the tenant, although tenants do not need to submit bids to exercise the RFR (see Table 1). These bids by right holders may constitute safety bids; that is, right holders may bid to avoid auction failure and potentially higher prices in a repeat auction or may mistrust the RFR mechanism. In 576 auctions when the right holders submitting a bid do not win, their bids are 64% of the winning bid on average (see Appendix Figure A2). In the same 576 auctions, 75.6% of the right holders subsequently exercise the RFR.

Table 1 also reports that tenants purchase in 59% of LGSA auctions by exercising the RFR and in 11% of the auctions by submitting the highest bid. Thus, non–right holders win 30% of the LGSA auctions. The share of right holder purchases varies across the number of participants: right holders purchase in 82.5% of the auctions with two participants compared with 59.2% in auctions with more than eight participants (see Appendix Table A2).

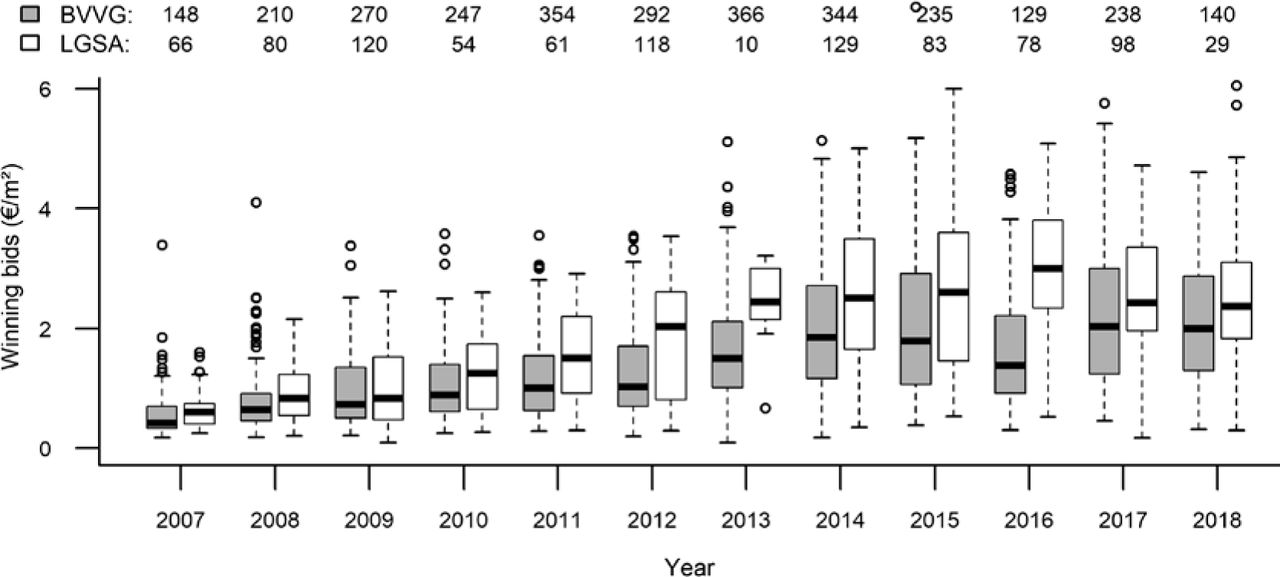

Auctions in which right holders bid successfully receive on average fewer bids (3.03) and lower prices (€1.03/m²) compared with auctions where tenants purchase by exercising the RFRs (4.59 bids; €1.83/m²) or reject using them (4.93 bids; €2.29/m²; Appendix Table A3). For LGSA, there are higher average (unconditional) winning bids, with an average of about €1.88/m² compared with €1.45/m² for BVVG. Figure 3 shows the variation by seller over the observation period.

Winning Bids and Number of Observations (top) of BVVG and LGSA Land Auctions 2007–2018

From 2007 to 2018, average winning bids increase by around 270% for both sellers, which is in line with observed price surges for farmland in Germany and Saxony-Anhalt (e.g., Hüttel, Wildermann, and Croonenbroeck 2016; Grau, Odening, and Ritter 2020; Ritter et al. 2020). Although absolute differences in winning bids between LGSA and BVVG are small in 2007 (€0.64/m² and €0.59/m²), the gap widens to €2.59/m² for LGSA and €2.11/m² for BVVG, respectively, in 2018.

4. Empirical Approach

Strategy

LGSA and BVVG share the same auction mechanism in the same market at the same time, although LGSA favors tenant bidders with the RFR. Testing the four conjectures requires us to estimate the effects attributable to tenant favoritism with the RFR in LGSA auctions on auction competition measures (C1a and C1b) and winning bids (C2a and C2b) compared with BVVG auctions. This implies comparing land auctioned under LGSA conditions with RFR (treatment group LGSA), and the same land auctioned without RFR (unobserved counterfactual). We rely on comparing land auctioned under BVVG conditions without tenant favoritism and RFR (control group). Adopting a double robust matching approach (Ho et al. 2007), we use nonparametric statistical matching in a first step to find comparable lots and retrieve the control group, and we use parametric postmatching regression analysis in a second step to estimate the effects attributable to tenant favoritism with the RFR.

Based on the matching approach, we identify the counterfactual group (control group) by conditioning on all confounding characteristics; that is, observable covariates other than the RFR that are relevant for the land auction competition measures and the winning bids (outcome measures), and whether the land is in one or the other auctioneer’s portfolio (selection into treatment). The matched control group then constitutes an unbiased source of information on what would have occurred in the counterfactual scenario if postmatching balance holds for all covariates (Imbens and Rubin 2015; Kainz et al. 2017) and conditional mean independence between outcome measures and treatment can be achieved (Imbens 2004).

Two-Step Procedure

In the first step, we preprocess the data relying on one-nearest neighbor matching based on the Mahalanobis distance, a proposed measure when there is a small number of covariates (Stuart 2010). This matching approach achieved the best postmatching covariate balance compared to two-nearest and three-nearest neighbor matching and kernel matching (see Appendix D for a summary of two-nearest and three-nearest neighbor matching and kernel matching results).

The set of conditioning covariates comprises hedonic variables, region, and time measures. We rely on the hedonic variables that describe land productivity: lot size (xs), soil quality (xq), and composition of the auctioned lot by respective share of arable (xa) and other land (xo), such as fallow land without a specific usage type. These hedonic variables denote typical price determinants; for instance, the higher the soil quality, the higher the productivity (Nickerson and Zhang 2014). Larger lots are more expensive than medium to small ones because farming them may benefit from economies of scale. Larger lots with higher shares of arable land and soil quality may attract more bidders (Croonenbroeck, Odening, and Hüttel 2020). Small lots, however, have been sold at higher prices. This can be attributed to location and buyer types; for instance, land close to urban centers (e.g., for keeping horses) may attract more nonfarmer bidders with a high willingness to pay (Brorsen, Doye, and Neal 2015; Ritter et al. 2020).

Systematics of why a parcel is privatized by LGSA or BVVG mainly relate to previous ownership and location. We thus also match on region using the geocoordinates of the centroid of the local subdistrict (Gemarkung), where a lot is located, to condition on a chief determinant for an auctioneer’s “selection” of a lot.

Given land markets’ thinness, matching on region may also reduce bias from local land market specificities and the microstructure that may influence bidder participation and sale price (King and Sinden 1994; Cotteleer, Gardebroek, and Luijt 2008). When potential bidders anticipate the number of potential buyers and sellers in a region, it may influence their expectations about future substitute land offers and their decisions to participate (Seifert, Kahle, and Hüttel 2021). By matching on region, we capture local weather conditions, such as water availability. For Saxony-Anhalt, which mainly relies on rainfed agriculture with yields subject to drought risks (Schindler et al. 2007), expected weather conditions and drought risks are likely to affect bidders’ expectations about future returns and thus price formation (Chatzopoulos and Lippert 2015). Matching on a fine-grained regional scale, however, prohibits us from comparing auctioned lots under different local land markets and climatic and weather conditions.

To account for the farmland price surge in the study period (Figure 3), for LGSA auctions in year t, we consider only BVVG auctions in [t − 1; t + 1] as potential matches. Because a BVVG auction can serve as a match in up to three time corridors, the matching procedure ultimately corresponds to matching with up to three replacements.

To achieve conditional mean independence, we further need to rule out unobserved confounders, particularly unobservable selection into “treatment.” Unobserved confounders include previous uses of the land that may affect future productivity and relate to the leasing contract with the respective agency; costly crop rotations, including catch crops or P-fertilization strategies that may only pay out for farms with longer lease contracts terms (Leonhardt, Penker, and Salhofer 2019); or unclear ownership that may hamper farm investments in such long-term soil productivity improvements. Lease terms or strategies do not seem to differ systematically by agency (e.g., before privatization, LGSA and BVVG used long-term contracts to prevent land from becoming fallow).

In the second step, we use the results of the matched sample consisting of treated and matched controls from the first step and run postmatching regressions. To analyze the competition effects  , we rely on a count data model. To retrieve the price effects

, we rely on a count data model. To retrieve the price effects  , we use a hedonic price model. Netting out the effects of tenant favoritism on competition helps us understand the role of the deterrence effect, particularly when tenants submit bids despite the missing incentive.

, we use a hedonic price model. Netting out the effects of tenant favoritism on competition helps us understand the role of the deterrence effect, particularly when tenants submit bids despite the missing incentive.

To test for the RFR effects on competition measures  , we consider that right holders submit a bid in 73% of LGSA auctions. While the bids may be “safety bids” submitted with no intent to win, we are unable to identify whether the right holders submit noncompetitive bids. Therefore, to characterize competition in auction i, we construct two outcome measures: (a) number of bids ni submitted to the auctioneer. In 73% of LGSA auctions, the number includes bids by tenants as right holders (see Table 1); and (b) number of bids by non–right holders,

, we consider that right holders submit a bid in 73% of LGSA auctions. While the bids may be “safety bids” submitted with no intent to win, we are unable to identify whether the right holders submit noncompetitive bids. Therefore, to characterize competition in auction i, we construct two outcome measures: (a) number of bids ni submitted to the auctioneer. In 73% of LGSA auctions, the number includes bids by tenants as right holders (see Table 1); and (b) number of bids by non–right holders,  . For LGSA, this measure corresponds to the total number of bidders excluding tenants. This group should determine the price in an LGSA auction that can be matched by the tenant using the RFR (see Burguet and Perry 2009). For BVVG, our second measure is identical to the number of bidders.

. For LGSA, this measure corresponds to the total number of bidders excluding tenants. This group should determine the price in an LGSA auction that can be matched by the tenant using the RFR (see Burguet and Perry 2009). For BVVG, our second measure is identical to the number of bidders.

Both competition measures are nonnegative integers with rare realizations of large numbers suggesting count data modeling. We note that a variance of the measures greater than their respective means (see Appendix Figure A3) prohibits using standard Poisson regression models. To adjust for the overdispersion, we adopt a negative binomial regression (NB2) model where the competition measures n* = (n,nnRH) follow a negative binomial distribution f (n*;μ,θ) with mean μ and dispersion parameter θ (Cameron and Trivedi 2013, 81; Hilbe 2014, 131). This specification allows a wider shape than standard Poisson regression models (Hilbe 2014, 129).7

We incorporate our covariates in the model following Cameron and Trivedi (2013, 81) and specify an exponential mean function μ = exp(z′ βNB2), where βNB2 are the parameters to be estimated, and z is a vector of regressors including a constant and the hedonic characteristics lot size (xs), soil quality (xq), and shares of grassland (xg) and other land (xo). The share of arable land serves as the reference category. We capture the remaining spatiotemporal effects by dummy variables dl for county l with l = 1,…,30, and dummy variables dt for the sales year t of the auctioned lot with t = 1,…,12. We include an indicator variable, dLGSA, for which δLGSAthe parameter to be estimated, gives the respective effects related to tenant support with the RFR on number of bids (C1a), especially by non–right holders in the LGSA auctions (C1b).

In the empirical specification, we shift both competition measures by one to the left to account for the support of the negative binomial distribution that has a positive probability of values being zero. This approach is commonly used when analyzing auction count data that structurally exclude zero observations (Jaggia and Thosar 1993; Hattori 2010; Piet, Melot, and Diop 2021).

For competition measures n and nnRH, the corresponding model specifications in logarithmic form for each auction i are

![[3a]](/embed/graphic-6.gif) [3a]

[3a]

![[3b]](/embed/graphic-7.gif) [3b]

[3b]

where α denotes the intercept, γ denotes the respective parameters of the spatiotemporal dummy variables to be estimated, and h(.) summarizes the hedonic part, where we follow the same specification as in the hedonic pricing framework (see equation [4]).

To test for tenant support with RFR-related effects on prices (C2′s), we use the hedonic pricing framework and regress the winning bids normalized by size in €/m² on the hedonic and spatiotemporal variables. Based on the Box-Cox procedure (Davidson and MacKinnon 2004, 432), we rely on a log-linear model and consider lot size xs in squared form, and all other variables in linear form such that

4

4

We estimate the tenant support with RFR-related effects on the prices based on the coefficient related to the LGSA indicator variable dLGSA (C2a). To acknowledge that the prices vary by the number of bidders, we replace the intercept by six dummy variables dk related to the number of participants (Brannman, Klein, and Weiss 1987), where we categorized by k = 2,3,4,5,6–8,9+ participants to ensure at least 65 observations for each seller in each category indicated by dk. With u denoting the error term, the hedonic model for each auctioned lot i is

![[5a]](/embed/graphic-9.gif) [5a]

[5a]

To test for price effects varying with number of bidders, and with the attractiveness of the lots by soil quality and size (C2b), we interact the respective participant indicators dk with the LGSA dummy variable. This allows us to obtain competition-specific effects of tenant support with RFR on the price; the corresponding model for each auctioned lot i is

![[5b]](/embed/graphic-10.gif) [5b]

[5b]

We infer about this conjecture using four statistical tests: we use an F-test to test the statistical null hypothesis that all estimates of  are equal to zero. Second, using pairwise two-sided t-tests, we test the null hypotheses that respective estimates of

are equal to zero. Second, using pairwise two-sided t-tests, we test the null hypotheses that respective estimates of  are equal. Third, we use multivariate one-sided tests (Wolak 1987; Silvapulle and Sen 2001) to test whether the estimates of

are equal. Third, we use multivariate one-sided tests (Wolak 1987; Silvapulle and Sen 2001) to test whether the estimates of  are smaller for = 2, 3, 4, 5 than those for k = 6 − 8, 9 + participants, respectively. Following Vanbrabant and Rosseel (2020), we use a two-stage testing procedure based on F-tests. In the first stage, the null hypothesis

are smaller for = 2, 3, 4, 5 than those for k = 6 − 8, 9 + participants, respectively. Following Vanbrabant and Rosseel (2020), we use a two-stage testing procedure based on F-tests. In the first stage, the null hypothesis  ;

;  ;

;  ;

;  is tested against the alternative hypothesis that at least one inequality is violated. Because not rejecting the null hypothesis would include equalities, these are tested in the second stage. Fourth, based on the same testing procedure, we test for a decreasing order of LGSA effects with an increasing number of auction participants; that is, the null hypothesis in the first stage is

is tested against the alternative hypothesis that at least one inequality is violated. Because not rejecting the null hypothesis would include equalities, these are tested in the second stage. Fourth, based on the same testing procedure, we test for a decreasing order of LGSA effects with an increasing number of auction participants; that is, the null hypothesis in the first stage is  .

.

Finally, to investigate whether the auction results differ systematically between cases where the right holder does or does not exercise the RFR, or wins by its own bid, we modify model [5a] by replacing the LGSA dummy variable with three indicators: dER indicates that the right holder exercises the RFR, dRR indicates that the right holder does not, and dOB indicates that the right holder wins by its own bid. The resulting model is

![[5c]](/embed/graphic-11.gif) [5c]

[5c]

To account for having a control unit matched to multiple treated units (Ho et al. 2011), we implement weighted negative binomial regression models [3a] and [3b] and weighted least squares regression models [5a]–[5c] with weights on the control units proportional to their matching frequency. To account for potential heteroskedasticity, we base inference on robust standard errors (White 1980). We use the R package MASS (Venables and Ripley 2002) to estimate weighted negative binomial models by maximum likelihood procedures, the sandwich package (Zeileis 2006) to derive robust standard errors, and the MatchIt package (Ho et al. 2011) to implement matching.

5. Results

The one-nearest neighbor matching matches 926 LGSA auctions (treatment group) with 590 BVVG auctions (control group); 328 auctions match one time, 188 match two times, and 74 match three times. Matching results seem satisfactory regarding the covariate balance (Figure 4); the absolute standardized difference in means (see Figure 4a) is below the critical value 0.2 for all hedonic variables (Rosenbaum and Rubin 1985).8 QQ-plots (see Figure 4b–e) indicate common support on the covariate distribution between the treated and matched control samples (close to the 45-degree line). Matched auction pairs are on average 26.1 km apart, and 92.6% of the matches are in Saxony-Anhalt, which suggests satisfactory matches on location (see Appendix Figure A4 and Tables A4–A5 for the descriptive statistics).

Matching Quality Measures

Table 2 reports the results of the postmatching regressions (see Appendix B for the parameter estimates for county and year dummy variables). The negative binomial regression results for the competition measures (C1′s) based on models [3a] and [3b] reveal a satisfactory range of the pseudo R-squared (0.292 and 0.326, respectively). For effect size, we refer to an elasticity measure; that is, the proportional change in the expected mean of the competition measures induced by a change in the covariates by one unit while holding all other variables constant (Atkins and Gallop 2007, 731). Therefore, reported coefficients need to be transformed by exp(.)−1, where estimates smaller than 0.1 can be directly read as the proportionate change (Cameron and Trivedi 2013, 94).

Postmatching Regression Results

As expected, a better soil quality index, larger lots, and higher shares of arable land attract more bidders with comparable effect size across the models, for instance, increases in the soil quality index increased the number of bids (n) by 0.9% and the number of bids by non-right holders (nnRH) by 1.1%, respectively. On average and attributable to LGSA’s tenant support with RFR, we find 8.9% fewer n (e−0.093−1 = −0.089) and 28.7% fewer nnRH (e−0.338−1 = −0.287) submitted to LGSA. Based on robust standard errors, a z-test rejects the null hypothesis of zero δLGSA-coefficients at the 5% (n) and 1% (nnRH) level, respectively. The findings lend support to the competition and deterrence effects, C1a and C1b.

The hedonic price regressions (C2′s) based on models [5a]–[5c] reveal R-squared values of around 0.87, suggesting a satisfying model fit (see Table 2). The coefficient estimates of the participant class indicators suggest higher prices in auctions with more participants. Correspondingly, better soil quality, larger lots, and higher shares of arable land lead to higher prices.

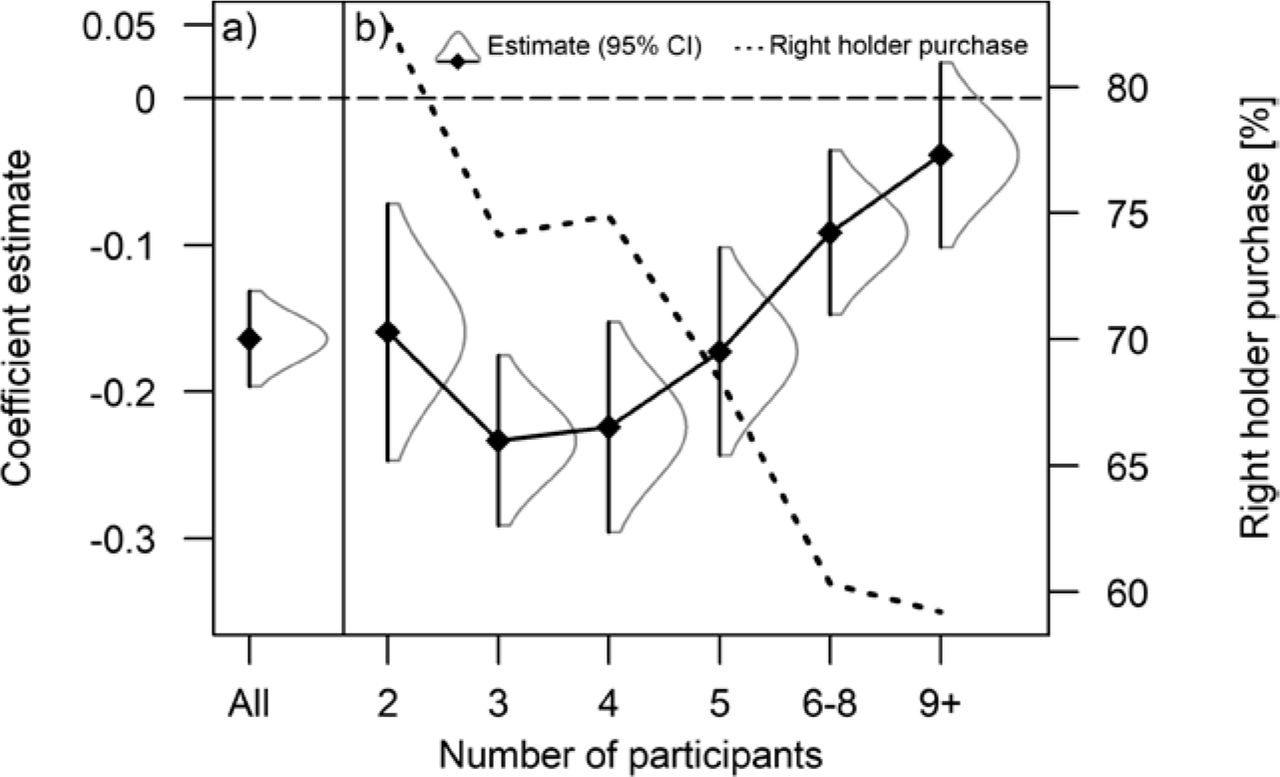

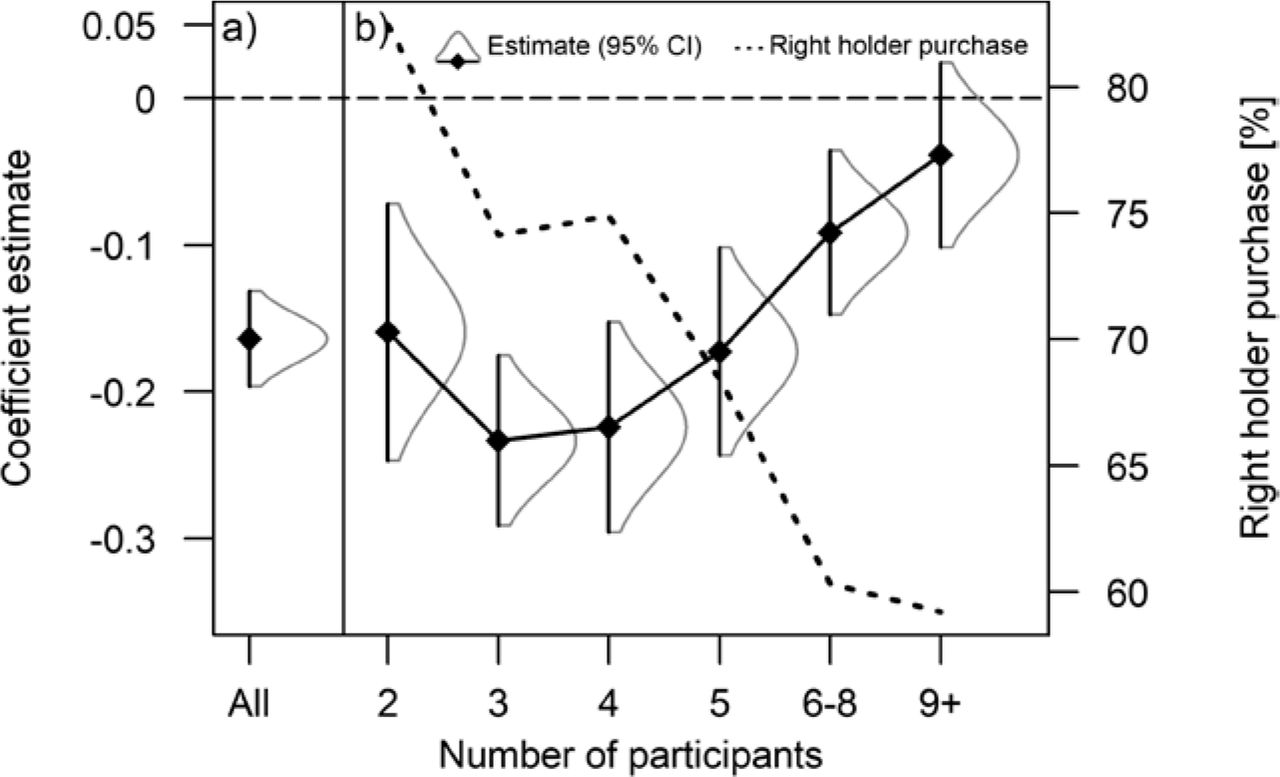

In all hedonic price regressions [5a]–[5c], t-tests based on robust standard errors reject the respective null hypothesis of zero estimated parameters for δLGSA, suggesting a negative price effect of LGSA’s tenant support with the RFR on winning bids. Based on model [5a], we find an average negative effect of about −16.4%. This lends support to a price effect of tenant support with RFR aligned to C2a (Figure 5a).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Rights of First Refusal–Related Price Effects over the Number of Participants Based on the Coefficients of Model Equation [5a] and [5b]

Results of model [5b] suggest a negative price effect related to tenant support varying across competition categories by number of auction participants (Figure 5b): Auctions with two participants show a negative price effect of about −15.9% related to tenant support with the RFR; for auctions with three up to nine or more participants, negative price effects are decreasing from −23.3% to −3.9%, respectively. For nine or more participants, the estimated coefficient shows large uncertainty by the standard error; thus, we infer that our data do not show statistically significant price differentials between sellers at these levels of competition.

Test results (Appendix Tables C1–C5) indicate that the coefficients for two, three, four, and five participants are statistically significantly smaller than the coefficients for nine and more participants and for six to eight participants, respectively. Multivariate one-sided tests provide statistical evidence that the price differences between the sellers are (weakly) decreasing as the number of participants increases (i.e., price effects related to tenant support with the RFR decrease as competition increases). This lends support to the asymmetry effect, C2b.

Model [5c] reveals that if the tenant exercises the RFR in LGSA auctions, the winning bids are about 16.8% lower on average compared with BVVG auctions without the RFR and 38.2% lower if the right holders win by own bids. This finding supports that right holders do submit noncompetitive safety bids. If the tenant does not exercise the RFR and a nontenant wins instead, the winning bids are about 5.6% lower on average compared to BVVG auctions without the RFR. In other words, more non–right holders are likely to win in auctions having more bidders. This finding lends support to the asymmetry effect, C2b (see also Appendix Tables A2 and A3).

6. Discussion

This study investigates whether granting an RFR to tenants reduces competition and final sale prices in farmland auctions in eastern Germany from 2007 to 2018. Using a double robust approach, we find a negative effect of about 8.9% on the number of overall bids submitted to LGSA auctions with RFR compared with BVVG auctions without RFR. This is in line with C1a and auction theory (Brisset, Cochard, and Maréchal 2020) and our assertion that under tenant favoritism with an RFR, right holders may not have an incentive to submit a bid. However, in our data, we observe that right holders seem to submit safety bids to avoid auction failure and potentially higher prices if the auction repeats; or they may mistrust the RFR mechanism. Although bids submitted by right holders add to the number of submitted bids as a measure of competition, they may have less price effect than bids submitted by non–right holders. We expect tenants to be aware that submitting unnecessarily high bids may increase prices and argue that the group of non–right holders is the price-determining group (Burguet and Perry 2009).

Our findings further indicate that non–right holders may be especially reluctant to submit bids compared to BVVG auctions (see model equation [3b]), where we find even a stronger RFR-related effect (28.7%) on the number of submitted bids submitted by this group. This lends support to a deterrence effect line with C1b. Ultimately, this suggests that the price-determining group is smaller in auctions with tenant favoritism under both a competition effect and a deterrence effect. This is also supported by the data: for LGSA auctions, non–right holders submit about 3.79 bids compared with about 5.15 bids submitted to matched BVVG auctions.

We find that the core land characteristics affect competition measures and winning bids; for instance, high-quality soils attract more bidders with a higher willingness to pay, a known factor in Saxony-Anhalt (Seifert, Kahle, and Hüttel 2021). Likewise, larger lots with a higher share of arable land attract more bidders and achieve higher prices (Ritter et al. 2020; Piet, Melot, and Diop 2021). Farmer bidders may benefit from economies of scale by larger plots, and nonfarmer buyers intending to generate income from leasing the purchased land may benefit from finding solvent farmer-tenants at a lower cost (Hüttel et al. 2020; Curtiss et al. 2021).

The net price effects associated with granting RFRs to tenants, however, need to be viewed by the level of competition (Figure 1). Hence, our hedonic models (equations [5a]–[5c]) include the intercepts related to the number of auction participants. Across all models, we find a robust positive relation between winning bids and auction participants. This is consistent with auction theory, indicating a response by bidders to more expected competition (Krishna 2009) and empirical studies using reduced-form models in the land market context (Hüttel et al. 2013).

Netting out the price effects related to competition reveals a negative direct average price effect of LGSA’s support for tenants of about 16.4% (model equation [5a]), and lends support to C2a. The estimated effect size seems plausible compared with Hüttel, Wildermann, and Croonenbroeck (2016), who observe higher prices by LGSA and BVVG compared with the search market, but lower for LGSA (€0.19 and €0.10/m², respectively). The authors, however, only use data from 2009–2010, and their comparison does not allow interpreting the differences as causal effects of tenant favoritism.

Linked to the different competition categories described by the number of participants (model equation [5b]), tenant support with RFR-related price effects decrease with more participants, lending support to an asymmetry effect, C2b. Non–right holders may bid more aggressively under the RFR particularly for attractive lots that attract more bidders reacting to the RFR and compensating for their (perceived) disadvantage. Another reason might be that competition and effects related to an adjusted bidding strategy appear simultaneously, where the absence of the right holder’s competitive bid (competition effect) becomes most effective in auctions attracting few bidders (Figure 5).

Differentiating the price effects by right holder behavior (model equation [5c]) reveals that tenants win by own bids at lower prices of about 38.2% on average in LGSA auctions compared with BVVG auctions. LGSA auctions in which tenants win by own bids usually are auctions with a low number of participants (two to four participants in 91% of the auctions; see Appendix Table A2) and are likely subject to the deterrence effect of the RFR. The effect may be especially pronounced for less attractive lots based on (unobserved) characteristics other than size and quality, such as lack of accessibility. Likewise, we find that right holders win by exercising the RFR at on average 16.8% lower prices.

Hüttel, Wildermann, and Croonenbroeck (2016) also find that LGSA sells to local farmers at lower prices compared with mean search market prices. Their finding supports our assumption that bids by right holders may be safety bids instead. Figure 5 reveals that tenants reject using the RFR when prices are high in auctions having more participants. This behavior is known as the right holder’s buy-refuse decision under unfavorable conditions (Choi 2009).

Overall, this suggests that this favoritism enables tenants to buy at lower prices without search costs. Tenants may further benefit from the RFR because this option to buy generates planning security, an issue especially relevant for the strategic development of farms (Higgins et al. 2018), and mitigates the risk for tenants losing their land in the privatization process. While this contributes to stabilize local farms, defining “local” remains challenging in this prospect (see Plogmann et al. 2022), and no guarantee exists that right holders buy at advantageous prices but resell to investors. Furthermore, we find evidence of a deterrence effect that may actually apply to investors or other local farmers, limiting their development options, and start-up possibilities of others.

Our results have the following implications: because privatization agencies constitute major players in eastern Germany’s farmland markets (see Appendix Table A1), these auction results appear in land price data publications. The information often serves as a benchmark for forming bids, for potential buyers and sellers, and influences the bargaining process in the search market (Seifert, Kahle, and Hüttel 2021; Balmann et al. 2021). Compared with the search market, lower LGSA prices when tenants exercise the RFR, or higher prices for attractive lots with many bidders may therefore bias expectations without knowledge about the “true” local price formation process (Bigelow, Ifft, and Kuethe 2020). Therefore, we recommend increasing market transparency by showing how the (privatization) auction results are determined.

Although all interested bidders can participate and the RFR is in line with EU legislation, our findings indicate that tenant support in privatization auctions comes at the cost of competitiveness, potentially discrimination against non–right holders, and forgone revenue derived from privatization. Given a transaction volume of €133 million for our LGSA sample and the average RFR effect of −16.4%, a back-of-the-envelope calculation suggests a loss of revenue of about €26 million. To prevent low prices, the auctioneers may publish a communicated reservation price in combination with the RFR. If, however, there are reasons to maintain size and increase ownership by local farmers to ensure more sustainable land management and to achieve other societal and environmental objectives (Eder, Salhofer, and Scheichel 2021; Stevens 2022), tenant support by granting RFRs may be defensible. To our knowledge, whether ownership fosters sustainable land management is still debatable (see Leonhardt, Penker, and Salhofer 2019). There seems to be no evidence for our study region, and we suggest this for future research.

Our results are transferable to comparable auction contexts, where a special relationship between the auctioneer and bidder groups exists. An example denotes a longtime service supplier in procurement auctions, where favoritism is not necessarily made explicit by granting RFRs (Laffont and Tirole 1991). In some European land markets, irrespective of the market mechanism, RFRs for local, neighboring, or tenant farmers are granted, and in Germany, where the right can be exercised by rural settlement agencies in case a local farm is willing to pay the price and can demonstrate its need for additional land (Galletto 2018; Moog and Bahrs 2021). Therefore, our results are not directly transferable to these land markets and other segments of the German markets because the chance that the right is exercised seems lower due to administrative burden.

We note the following limitations of our study. First, unobserved heterogeneity between sellers and why a lot appears in one or the other seller’s portfolio may confound the estimated causal effect of tenant support. Likewise, bidders may prefer one auctioneer over the other (sample selection bias) due to, for example, bid preparation costs varying by seller for reasons unrelated to the RFR, and differing secret reservation prices influencing the chance of repeating the auction. Given the limited land supply and overall market thinness, substitutes are limited, and we expect such bias to be low. Second, in a land market environment where local farmers as right holders can be described as competitive against other participants (Croonenbroeck, Odening, and Hüttel 2020), RFR-related effects may be sensitive to a right holder’s characteristics, such as the holder’s financial constraints, but our data did not supply this information. Third, although our reduced-form approach seems suitable for identifying net effects of tenant support and testing theoretical predictions of auction theory (Hendricks and Porter 2007, 2078), a structural estimation approach may help us better understand all bidders’ behavior.

7. Conclusion

Our study provides the first empirical evaluation of granting RFRs to tenants in land privatization auctions and the qualitative support to strengthen local farms. We use the region of Saxony-Anhalt in eastern Germany, where two privatization agencies differ in supporting tenants by granting RFRs and supplying qualitative information. Based on a double robust matching approach combined with regression models, we demonstrate that tenant support with RFR decreases the total number of submitted bids by 8.9%, particularly by deterring non–right holders (−28.7%), and reduces final sales prices by 16.4% on average. We conclude that granting RFRs supports tenants as local farmers, although at the cost of forgone revenues in privatization auctions; for our sample, we estimate a loss of €26 million. We suggest communicating a reservation price to increase market transparency and reduce bias in expectations when bidders form their bids. Future research should investigate whether local farms are really better land managers than larger, nonlocal or investor-owned farming enterprises when it comes to achieving societal and sustainability goals.

Acknowledgments

The authors gratefully acknowledge financial support from the University of Bonn and the German Research Foundation through Research Unit 2569 “Agricultural Land Markets: Efficiency and Regulation.” We thank the Landgesellschaft Sachsen-Anhalt mbH and the Bodenverwertungs- und -verwaltungs GmbH for providing data.

Footnotes

Appendix materials are freely available at http://le.uwpress.org and via the links in the electronic version of this article.

1 Examples include the 2003 Saskatchewan Farm Security Act (Ferguson, Furtan, and Carlberg 2006; Lawley 2018), direct farmer-neighboring owner’s preemption rights in Italy (Galletto 2018), and preemption rights granted to local farmers in Germany (Moog and Bahrs 2021).

2 A potential common component in bidder’s valuations is demonstrated by Seifert and Hüttel (2023). While a bidder’s estimate of the potential returns from landownership may depend on individual characteristics, the unknown future resale value is common to all bidders. The more optimistic a bidder estimates this value, the higher the bidder may rate the land’s current value.

3 This type of buy-refuse decision by the right holder of the RFR is comparable to a decision of a dishonest bidder in an auction under corruption (i.e., after submitting the bid, the dishonest bidder can revise it against a bribe payment) (Burguet and Perry 2007; Arozamena and Weinschelbaum 2009; Lengwiler and Wolfstetter 2010).

4 Appendix Figure A1 shows the overall transaction volume of LGSA and BVVG of utilized agricultural area by county.

5 Germany’s official soil quality index rates the valuation of field productivity by number of points and unifies pedologic, scientific, and economic factors in a unitless measure. Low (high) numbers indicate low (high) productivity.

6 Saxony-Anhalt totals 1,655 Gemarkungen of 12.36 km² on average.

7 The full density of the negative binomial distribution is given by f (n*|μ,α) = (Γ(n* + α−1) / (Γ(n* + 1)Γ(α−1)))(α−1 / (α−1 + μ))α−1(μ / (α−1 + μ))n*, where Γ(.) denotes the gamma function, and α is the inverted specification of the dispersion parameter θ (Cameron and Trivedi 2013, 81; Hilbe 2014, 131).

8 The standardized difference in means is defined as

, where

, where  and

and  denote a covariate’s sample mean in the treated and control groups, respectively, and

denote a covariate’s sample mean in the treated and control groups, respectively, and  and

and  are the corresponding sample variances.

are the corresponding sample variances.

- © 2023 by the Board of Regents of the University of Wisconsin System

This open access article is distributed under the terms of the CC-BY-NC-ND license (http://creativecommons.org/licenses/by-nc-nd/4.0) and is freely available online at: http://le.uwpress.org